If you run a limited company, you almost certainly pay yourself a combination of salary and dividends. The salary is paid as an employee of your own company; the dividends are paid out of the company's post-corporation-tax profits as a return on your shareholding. This combination is more tax-efficient than taking a large salary alone — but the optimal split depends on your specific circumstances, and the numbers shift slightly every year as thresholds and rates change.

This piece sets out how to think about the decision for 2025/26, the key thresholds involved, and the factors that change the calculation for different directors.

Why salary and dividends rather than salary alone

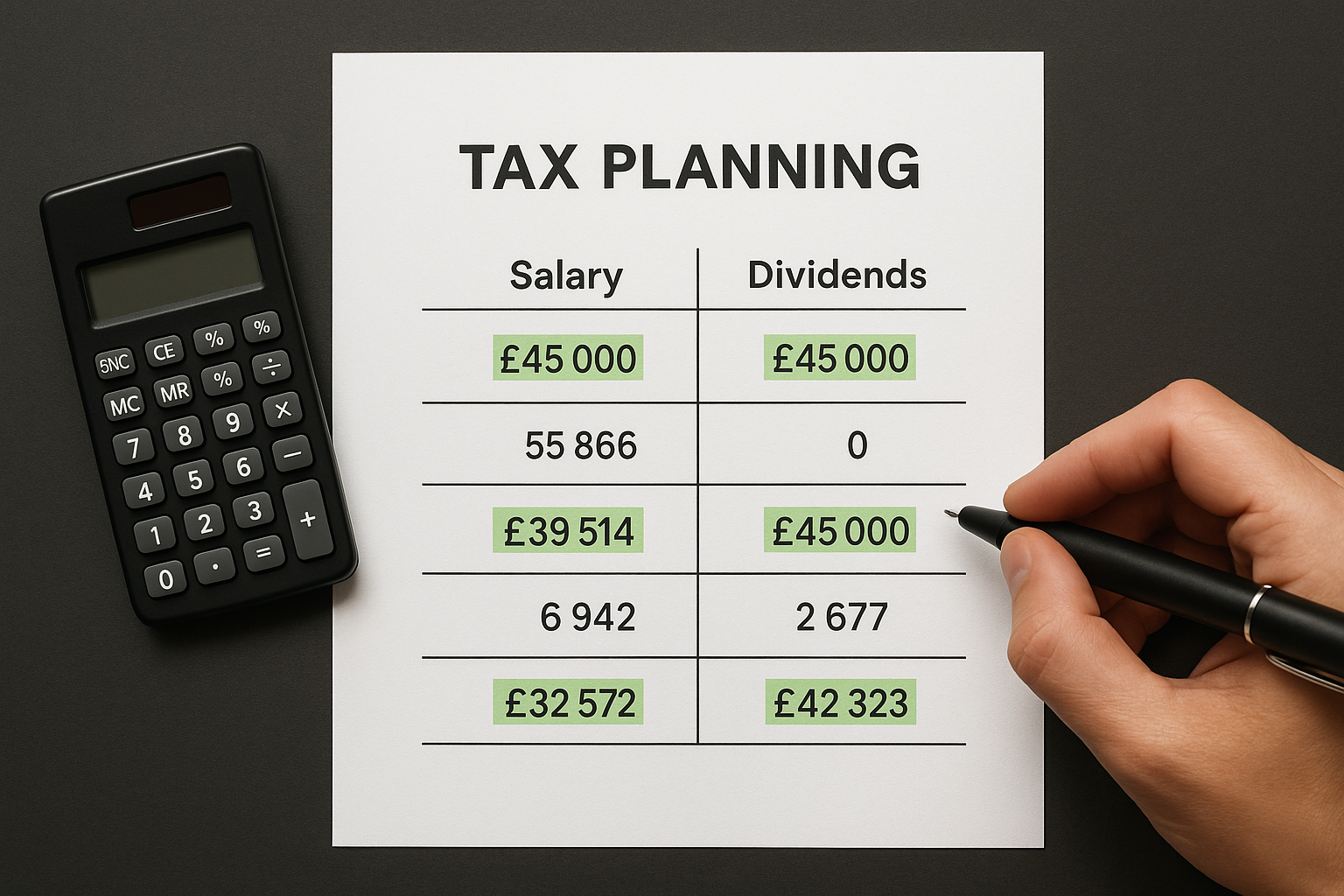

The core reason for taking a low salary and topping up with dividends is national insurance. Salary is subject to employee NIC (at 8% between £12,570 and £50,270 in 2025/26) and employer NIC (at 15% above the secondary threshold of £5,000 — reduced from £9,100 from April 2025). Dividends are not subject to NIC at all. This means that for income above the personal allowance, dividends are typically taxed at a lower combined rate than salary.

Corporation tax is paid on the profits before dividends are declared, which means dividends come out of post-tax profits. The effective combined rate — corporation tax on the profit plus dividend tax on the distribution — is still lower than the equivalent salary plus NIC cost for most directors. But the difference narrows as income increases, and it disappears or reverses in certain situations.

The key thresholds for 2025/26

Understanding the numbers requires knowing the relevant thresholds. For 2025/26:

- Personal allowance: £12,570 — income below this is free of income tax

- Secondary NIC threshold: £5,000 — employer NIC at 15% applies on salary above this

- Primary NIC threshold: £12,570 — employee NIC applies on salary above this

- Dividend allowance: £500 — dividends below this are tax-free

- Basic rate band: up to £50,270 — dividends in this band taxed at 8.75%

- Higher rate threshold: £50,270 — dividends above this taxed at 33.75%

- Personal allowance taper: begins at £100,000 adjusted net income

- Employment allowance: £10,500 — allows eligible employers to offset employer NIC

The standard optimal salary — and when it changes

For most owner-directors in 2025/26, the starting point is a salary of either £5,000 or £12,570, with dividends making up the rest of the income needed.

The £5,000 salary sits just at the secondary NIC threshold, meaning no employer NIC is triggered. It preserves a qualifying year for state pension purposes. The downside is significant — it leaves £7,570 of personal allowance unused, and it's a meaningful reduction from the previously optimal £9,100 level. For directors with no employment allowance available, it remains the cleanest option to avoid employer NIC entirely.

The £12,570 salary uses the full personal allowance — no income tax is due on it. However, it triggers employer NIC at 15% on the amount above £5,000, a cost of roughly £1,135 for the company (up considerably from previous years due to both the rate increase and the lower threshold). Whether this is worthwhile depends on the corporation tax deduction it generates. At 19% corporation tax, the deduction on the salary partially offsets the NIC cost, but the maths is tighter than it used to be.

If your company is eligible for the employment allowance — which offsets up to £10,500 of employer NIC — the calculation shifts significantly. With the allowance available, taking a salary of £12,570 becomes more tax-efficient, because the employer NIC cost is absorbed by the allowance and the full personal allowance is used.

The employment allowance is not available to companies where the sole employee is also a director. If you have at least one other employee paid above the secondary NIC threshold, the allowance is typically accessible — and at £10,500 it's now more valuable than ever given the higher NIC rate.

Dividends: what determines the rate paid

Once salary is set, dividends fill the remaining income requirement. The tax rate on dividends depends on which band they fall into after salary has been taken into account. For 2025/26:

- Dividends within the basic rate band (up to £50,270 total income): 8.75%

- Dividends in the higher rate band (£50,271 to £125,140): 33.75%

- Dividends above £125,140: 39.35%

For a director taking a salary of £9,100 and filling the rest of their basic rate band with dividends, the total income they can extract at basic rate tax rates (plus the corporation tax already paid on the profits) is significant — and the overall tax burden is materially lower than it would be on an equivalent employed salary.

The jump to 33.75% on dividends in the higher rate band is steep. For directors extracting income above £50,270, the tax efficiency of dividends versus salary narrows considerably, and pension contributions become an increasingly attractive alternative to taking the income at all.

Factors that change the calculation

The standard advice — low salary, dividends to fill the basic rate band — applies to many directors but not all. Several factors change the calculation:

Mortgage applications

Lenders assess affordability based on income. A director taking £9,100 salary and £40,000 in dividends may find some lenders will only count the salary, or use a multiple of salary plus dividends calculated differently to an employed applicant. If a mortgage application is on the horizon, it's worth understanding how your lender treats director income before optimising purely for tax efficiency.

Multiple shareholders

If the company has multiple shareholders, dividends must be declared in proportion to shareholding. If you want to pay different amounts to different shareholders, alphabet shares (different share classes with different dividend rights) provide flexibility — but need to be set up correctly and used appropriately to avoid the settlements legislation treating the income as yours regardless.

Income approaching £100,000

The personal allowance tapers at £1 for every £2 of adjusted net income above £100,000. In the £100,000 to £125,140 band, the effective income tax rate on the tapering portion is 60% — because each £1 of income costs £1 in tax, plus withdraws 50p of personal allowance which is then taxed at 40%. Pension contributions reduce adjusted net income and can partially or fully restore the personal allowance, making them exceptionally tax-efficient in this range.

Company profit levels

Dividends can only be paid from retained profits. If the company has had a difficult year and retained profits are low, the ability to take dividends may be constrained regardless of what the optimal tax split would be. Dividends paid in excess of distributable profits are unlawful and can create personal liability.

The honest bottom line

For most straightforward cases — sole director, no employment allowance, total income comfortably within the basic rate band — the optimal salary in 2025/26 is £9,100, with dividends making up the balance. The difference between taking £9,100 and £12,570 is small and depends on your corporation tax rate.

For anyone with more complex circumstances — multiple shareholders, income approaching higher rate thresholds, a mortgage in prospect, or significant retained profits to consider — the right answer requires a proper calculation rather than a rule of thumb. The numbers are close enough in some scenarios that individual decisions around pensions, other income, and timing can shift the optimal approach materially.

If you'd like to run through your specific position for 2025/26, get in touch — it's the kind of conversation that usually pays for itself.